/cdn.vox-cdn.com/uploads/chorus_asset/file/23962442/acastro_STK067__03.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/24016885/STK093_Google_04.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/24808816/Starfield__The_Settled_Systems___Supra_Et_Ultra_____Starfield__The_Settled_Systems___Su)

[ad_1]

Get FREE Sovereign Bond Updates

we will send you one myFT Daily Digest Latest Email Rounding sovereign bond News every morning.

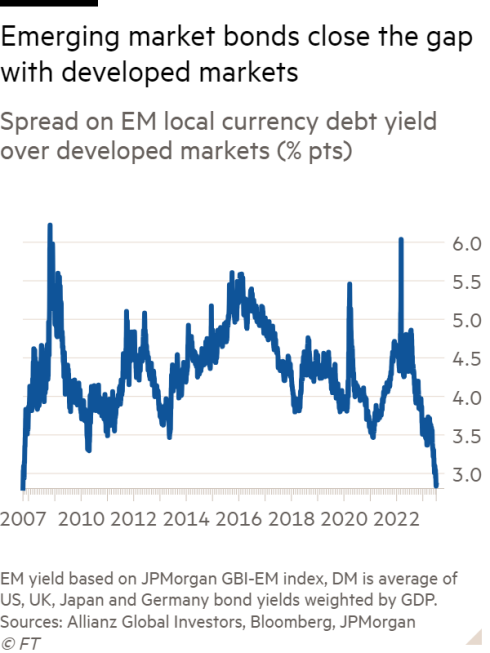

The gap in government borrowing costs between emerging and developed markets has narrowed to its lowest level since 2007, as investors anticipate imminent interest rate cuts in some major emerging economies and further tightening in the West.

The spread fell to less than 2.9 percentage points this week, the lowest in 16 years, from 4.8 points a year earlier, according to data from Allianz Global Investors.

“This year there has been a huge gap between local currency emerging market debt and developed markets,” said Richard House, chief investment officer for emerging market debt at Allianz Global Investors.

“Investors are underestimating the credibility gap between policy makers. , , Emerging markets have done a good job of handling this inflationary shock and I’m not sure you can say the same about some of the western central banks.”

Central banks in Latin America and Eastern Europe – the regions that are home to the best-performing bond markets in the world this year – are more likely to raise rates in response to inflationary pressures as economies reopen after the easing of coronavirus pandemic restrictions. Worked fast.

JPMorgan’s widely followed benchmark of emerging market local currency government bonds has delivered a total return of 7.5 percent so far, boosted by the Latin American sub-index, which rose 21 percent, and the Middle and Eastern by Europe, which has benefited. 11 per cent.

In contrast, US government bonds have delivered a total return of just 1.6 percent this year, as measured by the ICE Bank of America Index of Government Bonds, while German bonds – the de facto benchmark for the eurozone – have delivered a total return of 1.2 percent. Is. Hundred.

Given the still high real yields on offer in emerging market debt, waning inflation and the prospect of rate cuts, which should propel bond prices, many investors are positioning themselves to profit further.

“Local currency rates and bonds present a very attractive opportunity for the next six months and beyond,” said Liam Spillane, head of emerging markets debt at Aviva Investors. has underestimated the possibility of a rate cut.

Ian Steele, international chief investment officer for fixed income at JP Morgan Asset Management, said he expects emerging market local currency bonds to “continue to outperform given high real rates, central banks that are largely raising funds and declining inflation.” working with”.

“Our priority is for countries with high real rates such as Brazil, Mexico and Indonesia, as well as countries where we expect inflation to decline rapidly, such as the Czech Republic,” he added.

Economic prospects in the developing world also look relatively strong. In a recent note to clients, Bank of America forecast that emerging economies would grow at an average rate of 4.1 percent in 2024, higher than the 0.5 percent increase in the US, the widest growth gap in a decade.

The performance of local currency debt reflects relative resilience of some large emerging economies, which typically have deep local bond markets. Smaller and less developed emerging markets, which rely more heavily on foreign currency borrowings, have struggled this year as rising bond yields in the West have reduced the appeal of their dollar-denominated debt.

High US interest rates have put some countries dependent on dollar-denominated debt, including Pakistan, Tunisia and Egypt, under debt stress and close to default, according to David Honore, head of emerging market cross-asset strategy and economics at Bank of America. has reached. ,

“You have a very positive story that benefits mainstream, more liquid markets and at the same time you have a muted credit crunch in marginal markets,” Honor said.

[ad_1]

Get FREE Sovereign Bond Updates

we will send you one myFT Daily Digest Latest Email Rounding sovereign bond News every morning.

The gap in government borrowing costs between emerging and developed markets has narrowed to its lowest level since 2007, as investors anticipate imminent interest rate cuts in some major emerging economies and further tightening in the West.

The spread fell to less than 2.9 percentage points this week, the lowest in 16 years, from 4.8 points a year earlier, according to data from Allianz Global Investors.

“This year there has been a huge gap between local currency emerging market debt and developed markets,” said Richard House, chief investment officer for emerging market debt at Allianz Global Investors.

“Investors are underestimating the credibility gap between policy makers. , , Emerging markets have done a good job of handling this inflationary shock and I’m not sure you can say the same about some of the western central banks.”

Central banks in Latin America and Eastern Europe – the regions that are home to the best-performing bond markets in the world this year – are more likely to raise rates in response to inflationary pressures as economies reopen after the easing of coronavirus pandemic restrictions. Worked fast.

JPMorgan’s widely followed benchmark of emerging market local currency government bonds has delivered a total return of 7.5 percent so far, boosted by the Latin American sub-index, which rose 21 percent, and the Middle and Eastern by Europe, which has benefited. 11 per cent.

In contrast, US government bonds have delivered a total return of just 1.6 percent this year, as measured by the ICE Bank of America Index of Government Bonds, while German bonds – the de facto benchmark for the eurozone – have delivered a total return of 1.2 percent. Is. Hundred.

Given the still high real yields on offer in emerging market debt, waning inflation and the prospect of rate cuts, which should propel bond prices, many investors are positioning themselves to profit further.

“Local currency rates and bonds present a very attractive opportunity for the next six months and beyond,” said Liam Spillane, head of emerging markets debt at Aviva Investors. has underestimated the possibility of a rate cut.

Ian Steele, international chief investment officer for fixed income at JP Morgan Asset Management, said he expects emerging market local currency bonds to “continue to outperform given high real rates, central banks that are largely raising funds and declining inflation.” working with”.

“Our priority is for countries with high real rates such as Brazil, Mexico and Indonesia, as well as countries where we expect inflation to decline rapidly, such as the Czech Republic,” he added.

Economic prospects in the developing world also look relatively strong. In a recent note to clients, Bank of America forecast that emerging economies would grow at an average rate of 4.1 percent in 2024, higher than the 0.5 percent increase in the US, the widest growth gap in a decade.

The performance of local currency debt reflects relative resilience of some large emerging economies, which typically have deep local bond markets. Smaller and less developed emerging markets, which rely more heavily on foreign currency borrowings, have struggled this year as rising bond yields in the West have reduced the appeal of their dollar-denominated debt.

High US interest rates have put some countries dependent on dollar-denominated debt, including Pakistan, Tunisia and Egypt, under debt stress and close to default, according to David Honore, head of emerging market cross-asset strategy and economics at Bank of America. has reached. ,

“You have a very positive story that benefits mainstream, more liquid markets and at the same time you have a muted credit crunch in marginal markets,” Honor said.

{kind=link}